Give the Power of a Roth IRA

by Center for Personal Finance editors

The U.S. savings rate--as a percentage of disposable personal income--decreased from 10.5% in 1973 to just 2% in 2003.* Many people are asking how to encourage young people to save more of their income at an early age.

Roth IRAs (individual retirement accounts) are one solution. Some young people with earned income are realizing that a Roth IRA is a gift that keeps growing--long after graduation.

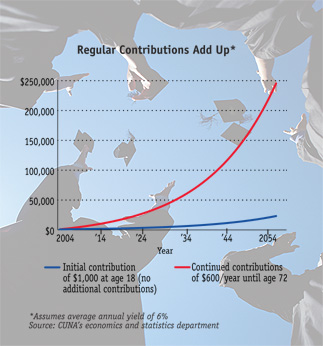

Consider this: If an 18-year-old high-school senior starts a Roth IRA with just $1,000, that investment will be worth more than $23,000 at age 72, assuming an average annual return of 6% over the long term with no additional contributions. If the graduate contributes just $600 a year for those 54 years, the investment grows to more than $245,000.

Know the rules:

There is no age requirement for a Roth IRA.

To be eligible for a Roth, anyone (including a child) must have earned income from a job; investment income, allowances, and money earned from chores do not count.

You only can make a gift equal to (or less than) the amount of the child's earned income, up to the $3,000 limit.

Experts recommend that grandparents or others interested in setting up a long-term savings plan make a gift to the grandchildren or their parents and let them open the account themselves.

Compound interest is a powerful tool, making a Roth IRA at graduation a gift that steers the young adult down a sensible savings path for life. Check with the credit union for more information.

Source: U.S. Department of Commerce, Bureau of Economic Analysis

May 31, 2004

|