CalculatorsTurn your dreams into reality. Use a calculator to figure out how to get where you're going financially. Whether you are wanting to know how much a loan payment will cost you each month or how much you should set aside for savings and investments to reach a future goal, our financial calculators are your resource.

These calculators are solely for informational purposes and provides reasonably accurate results; the calculations are not intended to be relied upon as actual borrowing/savings results computations. The use of these calculators is not a guarantee of credit.

Bankruptcy Abusers Hurt Everyone

Amy Manzetti

Every year, bankrupts wipe $44 billion in debts clean off the books, according to the National Consumer Bankruptcy Coalition in Washington, D.C. The cost of wiping away all this debt usually is passed on to you and other consumers, costing the average American household as much as $550 each year in extra credit costs. Nearly 10% to 20% of bankruptcy filers are taking advantage of the system--racking up debts and then filing bankruptcy to avoid paying them--even when they have the means to do so, according to the coalition.

Many people filing bankruptcy have no alternative due to unforeseen circumstances such as catastrophic medical expenses or loss of income. Still, too many affluent bankruptcy filers walk away from debts they could afford to repay. A proposed law--which may pass as soon as September--is about imposing some responsibility on people who can pay their debts.

The fact that the bankruptcy rate rose in the late 1990s during good economic times and remains high indicates to many that the system is being abused by people who actually are capable of repaying their debts.

Why is reform necessary?

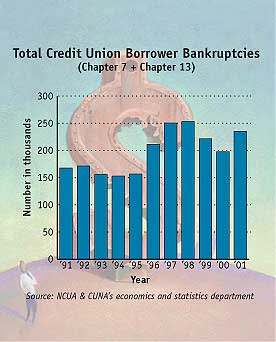

Nationally, credit union member bankruptcies rose 54% from 1994 to 2001. The Credit Union National Association (CUNA), the trade association for credit unions, estimates that half--$688 million--of all credit union losses in 2001 were due to bankruptcy. Credit union members as a whole pay for these losses in reduced dividends on shares, increased rates on loans, or less credit given than they otherwise would have been granted.

Credit unions are strong supporters of bankruptcy reform legislation because it will reduce the number of bankruptcy system abusers. For example, at Shoreline Credit Union in Two Rivers, Wis., a woman had an auto loan with her mother as a co-signer. The daughter fell behind on the payments, and the mother offered to take over the loan if the credit union was willing to remove the daughter's name from the loan. Since the mother had a good credit and employment history, the credit union agreed.

Former Enron Chairman Ken Lay could keep a $6 million apartment if he filed bankruptcy.

The mother filed for Chapter 7 bankruptcy before the first payment due date. The credit union lost $6,000 and eventually learned that the mother previously had filed for bankruptcy and didn't want her daughter to have the same credit problems.

While there are many changes proposed to current bankruptcy law, credit unions most strongly support protecting the ability of credit union members to voluntarily reaffirm their debts with their credit unions; including a meaningful "means test"; and including mandatory financial education provisions.

What bankruptcy reform means to you

Reaffirmation: Credit unions have a long history of working with members who declare bankruptcy. By voluntarily reaffirming debt (promising to pay the debt vs. discharging it in bankruptcy), members have the opportunity to work with a financial counselor to develop a plan designed to return them to sound financial standing. Also, by reaffirming with their credit union, members preserve their access to low-cost financial services and avoid paying rates of 25% or more from other providers.

According to Kenneth H. Beine, president of Shoreline Credit Union, "We had a middle-aged couple file for Chapter 7 in 1999 due to several medical problems and loss of employment. They reaffirmed their automobile loans with Shoreline. Although not required to repay their credit card loans, they were adamant about doing so, and did so quite voluntarily after discharge. Needless to say, today they are members in good standing, and need only ask to be granted future loans."

Means test: The proposed bankruptcy reform establishes an income-based "means test" to determine whether a debtor deserves to have some or all debts wiped away. The means test will determine whether a debtor can file for Chapter 7 bankruptcy, which erases almost all unsecured debt, or Chapter 13 bankruptcy, in which the debtor repays some or all debt under a repayment plan. Or, the court could order a debtor to pay those bills as promised.

Those who received financial counseling reduced their debt and improved their credit profile.

Almost two-thirds of consumers filing for bankruptcy do so under Chapter 7. If the means test comes into existence under bankruptcy reform, more debtors would have to file Chapter 13 bankruptcy.

Under the means test, if you have more than $100 a month left after paying approved expenses (no cell phones, no restaurant meals, and no movies), you will have to file Chapter 13 bankruptcy vs. Chapter 7 bankruptcy. The means test uses Internal Revenue Service living expense standards to determine which bankruptcy filing a debtor is allowed.

Mandatory financial counseling and education: Bankruptcy reform would require debtors to complete courses in personal financial management before their debts are discharged in bankruptcy. It allows debtors to explore their options, rather than automatically filing for bankruptcy.

Financial education needs to be available early on and before consumers experience financial problems. If you develop credit problems or are struggling to keep your finances in control, call or visit your credit union for help. Or contact The National Foundation for Credit Counseling (NFCC), Silver Spring, Md., at 800-388-2227.

Credit counseling works as both remedy and prevention to financial problems. Rather than filing for bankruptcy, which can scar your credit for years and limit your financial freedom, nonprofit credit counselors help you improve your financial situation.

Credit counseling positively affects consumer credit usage and payment behavior, according to a three-year study released by the NFCC.

Results of the study show that those who received financial counseling using the NFCC method reduced their debt and improved their credit profile over the three years--improvements in credit scores, fewer late payments, lower credit card balances, and less frequent use of credit lines. Bankruptcy costs the average American household as much as $550 each year in extra credit costs.

More changes

A few of the other proposed changes to bankruptcy law include:

Limiting repeat filings. A person currently can file for bankruptcy under Chapter 7 every six years, possibly changing to every eight years. A person currently can file for Chapter 13 bankruptcy as often as he or she wants (except, in some cases, not within 180 days of dismissal of a previous case), possibly changing to anywhere from two to five years;

Preventing debtors from reducing their outstanding debt load by switching their cases between bankruptcy chapters;

Placing a $1 million cap on the amount in Roth and traditional Individual Retirement Accounts (IRAs) that can be shielded from creditors, and protecting money saved in a Coverdell Education Savings Account, formerly called Education IRAs;

Requiring debtors to pay all charges made to credit cards in the three months prior to filing for bankruptcy; and

Enforcing a homestead exemption for all states. Currently, many states allow a debtor to keep possession of his or her residence (up to a certain limit) when filing for bankruptcy. Six states put no limit on the exemption for a primary residence.

For example, if former Enron Chairman Kenneth Lay were to file for bankruptcy under current law, he would be able to keep a $6 million apartment in Houston--why? Because of something in the current bankruptcy law called "unlimited homestead exemption." In Florida, Texas, Arkansas, South Dakota, Iowa, and Kansas, you can spend an unlimited amount of money on your primary residence, declare bankruptcy, and still get to keep the house no matter how lavish it is. Bankruptcy reform may change this exemption.

Consumers support bankruptcy reform

For the past three years, CUNA has asked voters if they favor or oppose requiring people who file for bankruptcy to pay off some of their debts if they are able to do so. Survey respondents (69%) strongly favor requiring people to pay off some of their debts if they can. Other CUNA survey findings show that the public strongly supports making it more difficult to declare bankruptcy.

Published August 5, 2002

|