June Financial Fitness Challenge�Power Through Credit Card Debt

Susan Tiffany, CCUFC

As signs of progress appear in the economy, there's growing concern about a new wave of credit distress�in credit cards.

Bank stress tests released in May 2009 suggest that the 19 largest U.S. banks could see almost $82.4 billion in credit card losses by the end of 2010, if what federal regulators called an "adverse economic situation" develops.

In fact, it's often a personal adverse economic situation�demise of a car engine, emergency family trip, medical bill for a pet�that leads many consumers to use credits card even when they're not the best choice. If you have no savings cushion, using a credit card may be your only choice, and thus the debt burden grows more crushing.

It's a classic trap: You can't pay with cash because you have no savings; you can't save because you must pay off credit card debts. That may account, at least in part, for why we carry an average of 5.3 all-purpose cards these days, and the average household credit card debt is $10,679, according to industry publication The Nilson Report.

Stop digging that hole

Your first priority when credit cards have the upper hand is to stop using them. This may not be possible if you're facing an unexpected, necessary expense. But you must stop any discretionary spending on credit. You must commit to this�or admit that you're not serious about ending your dependence on credit cards.

Then turn your attention to how you will pay off the bills. Take inventory:

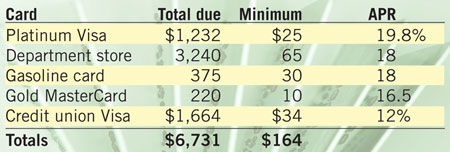

Identify how much you owe on each card.

Identify the APR (annual percentage rate) for each card.

Identify the minimum monthly payment for each card.

Add up all your credit card debts.

Add the total minimum monthly payments.

Here's a sample of what you might collect:

Next look at your spending plan and decide how much you can pay each month on all your credit cards. Let's say $300. Your next decision is how you will apply that amount to your credit card bills for the most effective payoff. There are two philosophies:

Pay off the smaller bills first.

Pay the bill with the highest APR first.

In either case, you always pay at least the minimum due�on time�on each card each month.

Choose your strategy

The rationale for paying the small bills first is to give you a sense of progress right from the get-go. In our example, you could wipe out two bills in about three months, while still keeping current on the other cards. Then you could continue paying down the balances on the three remaining bills.

The idea behind paying off cards in order of APR, high to low, is to make more progress on the debts that cost you the most. Just imagine, paying off a 20% APR credit card balance is like earning 20% on an investment�and that's a deal you won't find anywhere else these days. In this strategy, you make minimum payments on all but the bill with highest APR. You pay as much as you can on that bill from your monthly $300 credit card allotment. As you pay off each account, you continue to apply the same total each month to your cards, but transfer the largest payment to the card with the next highest APR.

Paying down a 20% APR credit card balance is like earning 20% on an investment.

You even could take a third approach and combine the two strategies. Pay off the small bills first, then tackle the remaining bills in descending APR order. This calculator can help you determine the payments you need to make to bury that credit card debt once and for all.

Financial Fitness Challenge

Credit card debt is certainly one of the prime financial fitness challenges consumers face these days. The people at your credit union can help you in this effort, in different ways.

For one, if you're carrying heavy debts, talk to someone at the credit union about getting back on track. Your credit union staff will either have a counselor you can talk to, or can refer you to someone they trust to help you and not make your situation worse.

And then, your credit union also is a safe bet to offer a better credit card, if you are eligible. In the wake of the new credit card legislation, much news coverage has noted credit union cards as exceptions to the bad actors in the market that spurred that legislation. You can count on a fair rate, low fees, and clear disclosure for a credit card from your credit union.

Please remember to register for the Financial Fitness Challenge. Each month we'll randomly select five winners to receive $50 Visa gift cards; we'll choose each month's winners only from that month's entries, so enter often.

ST

Susan Tiffany, CCUFC

[email protected]

Published June 8, 2009

|