Analyzing the Numbers: Getting a Handle on Small-Business Finance

Monica Steinisch

Many first-time business owners mistakenly believe that once they've put the financial data into the computer, they've done all it takes to get a handle on their finances. But inputting the data is simply the means to an end. The real value in those numbers lies in three tell-all reports--cash-flow statement, balance sheet, and income statement--that the figures produce.

"I truly believe that most of the small businesses that fail within the first five years do so because they didn't use their accounting software as a management tool," says Ted Hilliard, president of Hilliard Management Group and a trainer and consultant for the San Francisco Small Business Development Center (SBDC). "Using your financial reports means you can be proactive and make decisions that help you succeed."

Each of the three key financial statements provides a snapshot of your company's finances from a different perspective. Together, they paint a broad picture of your company's financial health.

Cash-flow statement

If there's one thing that can make or break an emerging business, it's cash flow. It's easy to get into a financial bind, particularly in the very early stages of launching a business, because often you'll have higher-than-usual expenses and just a trickle of income in the pipeline.

For example, a cash crunch could occur if your money is tied up in new inventory and you don't have enough cash left to hire a salesperson or pay to market your product. Another potential cash-flow problem could arise if a big, new client will pay you after you complete his or her project, but you won't have the cash to buy supplies or hire necessary subcontractors to get the work done.

As chief of the finance division in the San Francisco district office of the Small Business Administration (SBA), Ray Monahan sees firsthand what can happen when a business owner doesn't have a handle on business finances. "Many entrepreneurs mistakenly believe 'a sale's a sale,' without considering the cash-flow implications of the transaction," says Monahan. "In fact, how the money flows in and out of the business can make the difference between sinking and swimming."

"Most of the small businesses that fail within the first five years do so because they didn't use their accounting software as a management tool."

For example, the same business that fails because it pays cash for inventory on delivery and gives its customers 30 days to pay invoices could succeed if it paid for its inventory in 30 days and collected from its customers within 15.

Managing cash flow, or working capital, is essentially balancing your checkbook so you always have enough cash on hand to pay the bills. You accomplish that by estimating expenses and income over a certain period and planning how you'll deal with any expected shortfall. You'll be more likely to pre-empt problems if you closely monitor your cash flow and always know where you will stand in three months.

A cash-flow statement typically is made up of three sections:

Operating activities--all the usual daily business transactions that either use or generate cash, such as cash sales and interest earnings, and cash paid to employees and vendors.

Investing activities--transactions related to buying and selling equipment, real estate, and securities.

Financing activities--transactions related to such things as stock and bond issues and payment of dividends.

If, despite keeping a consistent and careful watch on your cash-flow statement, you find yourself in a bind, potential remedies might include borrowing money, arranging to pay some bills late, trying to collect on past-due accounts, and adjusting expenses. You also might change your policies going forward. For example, making it a policy to collect half the payment at the time of the sale and bill for the second half after delivery might solve some of your cash-flow issues.

Income statement

Also known as the profit & loss (P&L) statement, the income statement shows how profitable your business was over a particular time period. The calculation is as simple as:

"Using your financial reports means you can be proactive and make decisions that help you succeed."

sales revenue - expenses = profit or loss (also called net income or net earnings)

Obviously, a company can't survive if it never makes a profit, but showing a loss for a period doesn't necessarily spell doom. Negative net income might be the result of a seasonal fluctuation in the sales cycle or unexpected one-time expenses related to marketing or raw materials acquisition. Nonetheless, a positive net income over time is crucial to keeping your company solvent and growing. Comparing statements over time reveals trends about future net income.

The simplest income statement shows all of your normal revenues (those resulting from normal business operations) first, then all of your normal operating expenses. The difference between the two is your net income. Another section would be included after this line if you had any irregular income or expenses that were not the result of your regular business activities. This would be factored into the calculation for your final net profit or loss.

You would prepare a more complex P&L report if your business has a number of product lines. Breaking the numbers down to reflect income and expenses within specific areas allows you to see not only how the overall business is doing, but also how individual components affect the bottom line.

Balance sheet

The balance sheet compares the company's assets and liabilities, with the difference between the two being your equity. A series of balance sheets prepared at specific intervals can be quite telling, revealing trends that will influence your decision-making. For example, if sales have remained steady but receivables have gone up, you might decide to revisit your collection practices.

Your balance sheet will include three main parts:

The assets section will account for all the things of value that are owned or due to the business, including current assets (liquid investments, such as cash, stocks, accounts receivable, inventory, and prepaid expenses), fixed assets (such as land, buildings, vehicles, machinery, and equipment), and miscellaneous assets (such as the cash value of life insurance policies). Often omitted are intangibles, such as franchise rights, noncompete agreements, and patents because they are so difficult to value and may never be converted to cash.

If there's one thing that can make or break an emerging business, it's cash flow.

In the liabilities section, you'll list current liabilities (those due within a year, such as accounts payable, loans or credit due, and accrued expenses, such as payroll and taxes), as well as long-term debt (not due for at least a year) and stockholder/investor obligations.

Equity, or net worth, is what is left over after you subtract liabilities from assets. Liabilities and equity represent your company's sources of funding and together must equal the company's assets, which are the things the company invests its funding in.

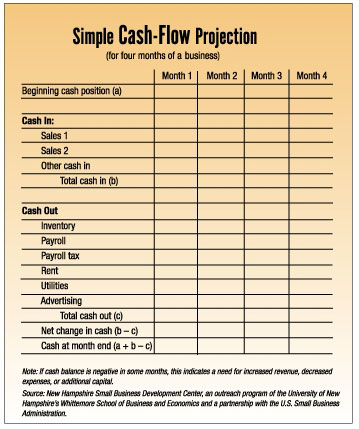

Cash-flow projection

The cash-flow projection is one of the most useful financial statements because it looks forward. The income statement and the balance sheet, to a large degree, illustrate what has happened in the past. While past experience is important, it is more important that you have an idea what the future holds and that you plan accordingly.

Assemble a cash-flow plan to budget your cash resources and to make sure expectations are realistic.

When preparing a cash-flow projection, remember:

Tailor the sample form (below) to your revenue categories and expense items.

Show payment of payables and collection of receivables when cash transactions actually happen.

Project cash flow usually for a 12-month period, or one fiscal year.

Published July 5, 2004

|