Highly Educated and Deep in Debt

by Amy Manzetti

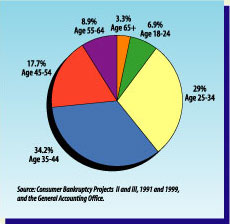

Consumers accounted for 97% of all bankruptcy filings in the U.S. in 2002, according to the American Bankruptcy Institute (ABI) in Alexandria, Va. In 2001, 9% of those applying for personal bankruptcy were younger than 25, according to a Visa Corp. survey. Seven years ago, only 1% of personal bankruptcies filed were by people 25 or younger.

Financial experts estimate that the shaky economy could force more than 1.5 million Americans into bankruptcy this year, and about one-third of them will be in their 20s and early 30s.

Why are so many young adults filing for bankruptcy? Maybe because 30% of college graduates enter the work force saddled with $10,000 to $25,000 in credit card debt and student loans, financial experts estimate.

Almost 28% of those surveyed by Nellie Mae, a national provider of higher education loans for students and parents located in Braintree, Mass., had combined undergraduate and graduate student debt of more than $30,000. For 22% of them, loan payments ate up more than one-fifth of their monthly income.

To support postcollege debt and other expenses, college graduates need to earn more than $38,000 a year. It's estimated that new college graduates may need up to six months to find jobs in their career fields; only 51% of college students have jobs by the time they graduate.

The good news: A 30-year-old today is 50% more likely to have a bachelor's degree than his or her counterpart in 1974 and earns $5,000 more per year, adjusted for inflation. However, he or she also has more in student loans and credit card debt, is less likely to own a home, and is just as likely to be unemployed. The future of Social Security for a 30-year-old today is unknown; a 30-year-old may have to depend almost completely on his or her own savings for retirement. Experts predict that many young adults will be in the work force longer than their parents in order to save enough for their retirement. Carrying a heavy debt burden always makes saving for retirement--or any goal--that much harder.

How the trouble starts

Credit cards are a leading cause of young adults' financial troubles. Student loans usually are manageable due to their low interest rates and extended repayment terms.

College students use credit cards for a variety of reasons: dining, clothing, books, tuition, fees, and other entertainment expenses. Approximately half of colleges allow students to charge tuition and fees, as well as other services. One of five students reports using credit cards to pay for tuition and fees.

"I started college in 1992 and almost immediately I was sent credit card offers," says Dionis, of Wisconsin, a respondent to our "What's Your Story" feature. "I tell you what, I didn't turn them down. I figured that when I did graduate, I would be making $45,000 a year and paying my credit cards off would be a cinch. Boy was I wrong. By the time I graduated college, I had almost $15,000 in credit card debt, and I was barely keeping up with the minimum payment amounts."

(We developed this article with input from readers contributing to What's Your Story.)

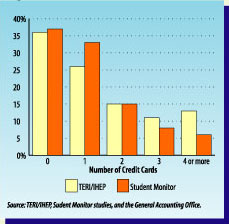

More than 80% of college students have at least one credit card by the end of their freshman year, according to Robert Manning, author of "Credit Card Nation: The Consequences of America's Addiction to Credit" (ISBN 0465043674). Of those, 25% received their first card in high school. Nellie Mae found that the percentage of college students with four or more credit cards hit 32% in 2000 and continues to rise.

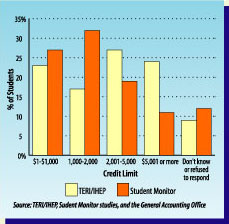

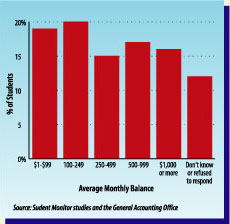

A Consumer Federation of America (CFA), Washington, D.C., survey says undergraduate students carry an average $2,000 balance, and one-fifth of students carry balances of more than $10,000. The CFA report indicates that many students are refinancing their debt either through student loans or with private debt consolidation.

Jennifer, of Georgia, got her first credit card when she was 18. "After that first card, I started getting preapproval offers from every credit card company imaginable. By the time I was 22, I was $5,000 in credit card debt."

Credit card issuers market to college students because they view them as good, new customers--although many college students have little to no income while in college.

Many universities allow credit card companies to solicit on campus grounds, considered by some to be part of the problem. Some alumni associations, athletic departments, and/or bookstores have relationships with credit card issuers, too, that allow issuers to solicit students.

| More than 80% of college students have at least one credit card by the end of their freshman year. |

Lack of financial education also is a problem contributing to young adults' financial troubles. The Jump$tart Coalition for Personal Financial Literacy's 2002 survey revealed high-school seniors are ignorant about personal finances. Overall, participants in the survey answered only 50.2% of the questions correctly. Jump$tart is a nonprofit provider of personal financial education programs based in Washington, D.C.

While it's easy to blame someone else, young adults can't ignore their own responsibility to educate themselves about managing credit. More than half of teens surveyed by the National Consumers League in Washington, D.C., mistakenly said that a credit card represents only an informal agreement to repay the debt.

Many credit card issuers provide consumer education on their Web sites, and the people at your credit union will be able to provide answers to your credit card questions. Also, some universities offer personal financial education during freshman orientation.

Suffering the consequences

The convenience of credit cards may tempt students to live beyond their means. Excessive credit card debt and late payments can impair a cardholder's credit rating and make it more difficult and costly to obtain credit in the future.

Students with high consumer debt are more likely to earn poorer grades, drop out of school, suffer from depression, file for bankruptcy, and work more hours to pay their bills. Credit card debt also has been linked to a number of suicides by college students, according to The Journal of Consumer Affairs, Auburn University, Ala.

Filing for bankruptcy often is seen as a way out of debt trouble to young people. However, many people who declare bankruptcy end up wishing they hadn't. They find out the hard way that:

More than 1.5 million Americans may declare bankruptcy this year; about one-third of them will be in their 20s and early 30s.

Bankruptcy mars your credit record. It stays on your credit report for 10 years.

You'll have a tougher time qualifying for future credit, such as an auto loan or a home mortgage.

All your financial obligations don't vanish with bankruptcy. You'll still owe alimony, child support, most taxes, and student loans.

Bankruptcy even might prevent you from getting a job, as employers sometimes check potential employees' credit reports.

| Thirty percent of college graduates enter the work force with $10,000 to $25,000 in credit card debt and student loans. |

A national credit-counseling expert says consumers pay more--a lot more--for credit after filing bankruptcy. Steve Rhode, president and founder of Myvesta.org, says families with clean credit pay an average of $1,100 each month for mortgage and auto loans. Because of higher interest rates, a postbankruptcy family pays almost $1,900 for the same items.

Chad, from Georgia, says he and his wife had to file for Chapter 13 bankruptcy--where the debtor repays some or all debt under a repayment plan--because they got into the "credit card craze" and accumulated up to $50,000 in debt. "Bankruptcy is a way out, but it's a very hard way. We know it's going to be very hard to rebuild from this, but we learned the lesson of money management the hard way," says Chad.

April 21, 2003

|