Following the Rules: Withdrawing From Your IRA

by Amy Manzetti

When you open an IRA (individual retirement account), you may think there's nothing more you need to do besides making annual contributions and accessing your money once you retire. However, if you don't plan ahead on how and when you should access your IRA money, you may get a worse tax bite than necessary.

The rules that govern minimum required distributions from IRAs are among the most complicated in our tax code. This article can only give an overview, so it's best to consult with an IRA specialist before making a distribution decision.

Required minimum distributions

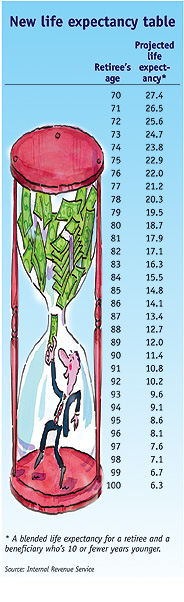

If you own a traditional IRA, you must start taking out a minimum amount of money by April 1 of the year following the year in which you reach age 70�--your required beginning date. You always can take out more, but not less than, the required minimum distribution amount. The required minimum distribution amount is based on a calculation of your account's value and your life expectancy--how many more years you are expected to live (see "What's your life expectancy?"). The longer your life expectancy, the lower the annual required distribution.

If you do not take at least the minimum required withdrawal each year, you'll owe a 50% penalty on the amount that should have been withdrawn.

Roth IRA owners are not required to take minimum distributions during the owner's lifetime. Roth owners can let their IRA grow free of federal taxes longer and take the money out on their own timetable.

Tax consequences of a withdrawalThe required minimum distribution amount is based on a calculation of your account's value and your life expectancy.

Dipping into your IRA, of course, means you'll also get stuck with an income tax bill. Traditional IRA funds are taxed upon withdrawal. At that time, according to Karen Yandell Buege, IRA training manager for CUNA Mutual Group in Madison, Wis., the owner must add the amount of the withdrawal to his or her income taxes for the year of the withdrawal.

For example, if your taxable income is $30,000 and you withdraw $5,000 from your traditional IRA, then you will pay taxes on $35,000 for that year. Owners who make nondeductible contributions do not pay taxes on that portion of their traditional IRA withdrawals.

Because Roth IRA contributions are not tax deductible, they are not taxed when withdrawn. Roth IRA earnings are taxable if the withdrawal is not a qualified distribution (see sidebar: Early withdrawal penalty exceptions). Contributions to a Roth IRA are withdrawn first, so no taxes are owed until the owner "dips" into earnings.

It's the IRA owner's responsibility to determine the taxable portion of each withdrawal, according to Buege, with assistance, if needed, from a professional tax adviser.

Calculating how much to withdraw

The amount of each required minimum distribution depends on your IRA account balance at the end of the previous year divided by a joint life-expectancy figure for you, the account owner, and your account beneficiary--even if you don't have a named beneficiary (see the life expectancy table). New minimum withdrawal rules automatically assume you've designated a person 10 years your junior as your IRA beneficiary if you haven't named one.

The rules that govern minimum required distributions from IRAs are among the most complicated in our tax code.

Your minimum distribution will change every year as your account balance and your life expectancy change. So you'll need to recalculate your minimum distribution amount every year.

What's your life expectancy?

The IRS (Internal Revenue Service) calculates your life expectancy based on its own tables. There are three different tables available, but you use only one to determine your annual minimum distribution for traditional IRAs. The IRS (Internal Revenue Service) calculates your life expectancy based on its own tables. There are three different tables available, but you use only one to determine your annual minimum distribution for traditional IRAs.

The uniform lifetime distribution table--this will be used by most IRA owners generally after reaching age 70 �, according to Ed Slott, certified public accountant in Rockville Center, N.Y. The only IRA owners who will not use this table are those whose spouse is their sole beneficiary and is more than 10 years younger than the IRA owner. Beneficiaries never use this table.

Joint life table--used only when the spouse is the sole beneficiary and is more than 10 years younger than the IRA owner. Beneficiaries never use this table.

Single life table--used by designated beneficiaries to compute required minimum distributions on inherited retirement accounts. This table is never used to calculate lifetime required distributions.

Roth IRA owners are not required to take minimum distributions during the owner's lifetime.

Life expectancy calculations can be complicated. Before you make any decisions, get expert advice.

June 16, 2003

|