Recovering From Identity Theft

Franny Van Nevel

Treva Welch always pays her bills on time and is careful not to abuse credit. So, the last thing this

24-year-old expected was getting turned down for a car loan last year because her credit report listed a $12,000 unpaid

cell phone bill. Soon afterward she got the news that she owed another $33,000 to a different cell phone provider.

After weeks of digging, she found that someone was using her name and Social Security number to open cell phone

accounts in Minnesota and Georgia—running up astronomical bills in her name. Welch was the victim of identity

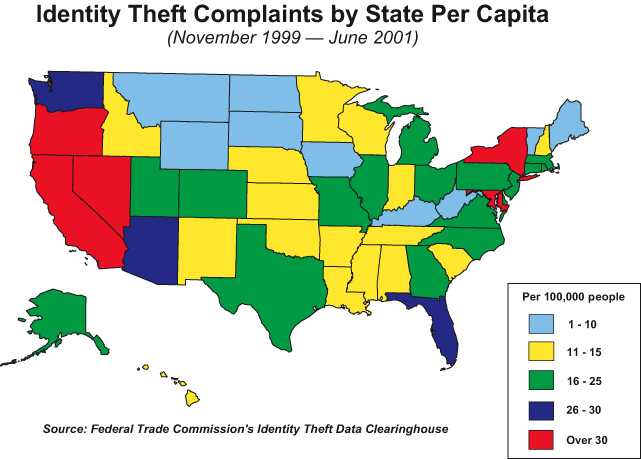

theft. According to the Federal Trade Commission (FTC), 204,000 consumers filed complaints about identity theft in

2001, making it last year's No. 1 complaint.

Anna Smith, Welch's co-worker, has an even more harrowing story. Smith bought a new car and before the first

payment was due she received a phone call telling her the car was going to be repossessed. After working her way

through a maze of deceit she discovered that a ring of thieves was using her identity across the country.

Six years later, she's still battling misinformation on her credit report and fending off creditors for the

remainder of the $90,000 damage done in her name. And for Smith, there was more than financial damage—the

thieves also obtained bogus drivers' licenses in her name in Illinois, Michigan, Nevada, and California.

|

Shred billing statements and any documents containing personal information before throwing them away.

|

Identity theft is a growing concern and costs creditors and consumers hundreds of millions of dollars each

year. Someone can use your name for years before you find out, and once you find out you face the lengthy and

expensive task of reclaiming your good name. According to the FTC, the average consumer spends more than $1,000 to

clean up the damage done by identity thieves. For many, the recovery process is painful and exhausting, but there

are steps to make it less odious.

Contact the three major credit bureaus

Explain your situation and ask that they put a fraud alert in your file. "The fraud alert is

a statement that says fraudulent applications for credit may be [being] made using your correct information," says

Dave Mooney, spokesperson for Equifax. It also instructs that you be contacted before any new accounts are opened

or existing ones changed.

At the same time, order copies of your credit report, which credit bureaus must give you free if your report is

inaccurate because of fraud. The bureaus worked with the FTC to design an "ID Theft Affidavit" that they will send

you or you can get by calling the FTC at 877-IDTHEFT or at its

Web site.

|

More than 200,000 consumers filed complaints about identity theft in 2001.

|

Once you get the reports, look carefully at three sections, says Jay Foley, director,

Identity Theft Resource Center

in San Diego. "First, check the information listed in the

header. If it shows you working for a company you've never worked for, or lists other addresses or P.O. boxes,

that's a red flag."

Next, check the primary section of the report, which contains information about open accounts or accounts

opened in the past seven years. Make note of any unfamiliar accounts. Then check the inquiries section, which

lists companies that are checking your report because they've received applications, says Foley. Request that

these inquiries be removed from your file and that any misinformation in the header be corrected.

Sadly, you might find a familiar address listed on your credit report. Foley says that in 12% to 17% of

identity theft cases, the victim knows the suspect, and of this group, 65% are estimated to be family members.

Victims then face the hard choice of turning a family member over to the police, or trying to work things

out—without outside intervention.

Contact creditors about fraudulent accounts

Mooney says that when a consumer calls

Equifax to report identity theft, Equifax gives the phone number of the fraud desk at any creditor. "They need to

call them right away and dispute it," says Mooney. The FTC advises consumers to follow up with a letter—the

procedure required by law—to resolve errors on credit card billing statements.

|

"Looking back I wish I would have just admitted what happened and asked for help, instead of relying on

myself."

|

Close any suspicious accounts and open new ones using new passwords and PINs (personal identification numbers).

Don't use easily available information like your mother's maiden name, your birth date, the last four digits of

your Social Security number, your phone number, or a series of consecutive numbers.

Ask your creditors if they'll accept the FTC affidavit and if they need a copy of your police report. Expect to

put in a lot of effort to get things straightened out. Welch says it seemed like it took forever to get the

misinformation off her credit reports. She had to fax a lot of information to creditors proving who she was and

where she lived. "It was so frustrating; it felt like the credit people were working against me, not with me."

Some consumers run up huge bills, however, and then "create" an identity thief to take the rap—so creditors'

caution is not always misplaced.

File a police report

Now you're ready to call your local police or sheriff's department to file

a report. Ask them to give you the report number and a copy of the report, which you'll need in order to get help

from creditors.

Create an ID theft case file

The Identity Theft Resource Center created a fact sheet called

"Organizing Your Identity Theft Case"

to help victims

become their own strongest advocates. This comprehensive how-to publication covers such areas as keeping good

notes in an organized journal, setting up an organized file system, and keeping track of expenses incurred while

working on your case.

"I wish I would have kept hard copies along with electronic copies of my files," says Anna Smith. Things she

thought were cleared up occasionally pop up, and she says she constantly has to dig for information. "Looking back

I wish I would have just admitted what happened and asked for help, instead of relying on myself."

|

Protect yourself

|

|

Don't give out personal information without knowing whom you're dealing with. If you must reveal personal

information, find out how it will be used and whether you can control how it's shared with others.

Shred all billing statements, ATM (automated teller machine) receipts, savings and investment account

statements, store receipts with an imprint of your credit card number, prescreened credit card or loan offers, and

any other documents containing personal information before throwing them away.

Don't use your

home mailbox or the postal out-basket at work to mail correspondence or bills that contain personal information.

Instead, deposit your mail in postal service collection boxes or at your local post office. Put a hold on your

mail when you travel.

Pay attention to billing cycles. If your bills don't arrive on time, contact creditors immediately to make

sure your account is secure.

Don't put your Social Security number on checks and don't carry the

card in your wallet.

Before ordering online,

check out the business' privacy policy and only

order from secure servers (the URL says "https" instead of "http" on the checkout screen).

Look over your credit card and bank statements each month

for unauthorized charges or suspicious activity.

If share drafts or checks you ordered don't

arrive when expected, notify the credit union.

Make a copy of all financial cards and insurance

cards you carry in your wallet (front and back) and keep it in a safe place. If your wallet is lost or stolen

you'll have all the information you need to promptly and accurately report the loss.

|

Published March 25, 2002

|